Commentary by Greg Davis, Vanguard chief investment officer

Events in Ukraine are creating a human toll and immeasurable suffering. Economic responses, including sanctions, have led to market turmoil and anxiety about what may come next. An emotional reaction is natural.

When it comes to investing, however, it’s best to resist the urge to act. It’s not easy, but in a situation such as this, we suggest investors steel themselves for what may come and try to keep emotions out of investing decisions.

Vanguard has studied more than two dozen geopolitical events of the past 60 years, some of which roiled the markets, to offer some perspective on how financial markets could react over the coming weeks and months.

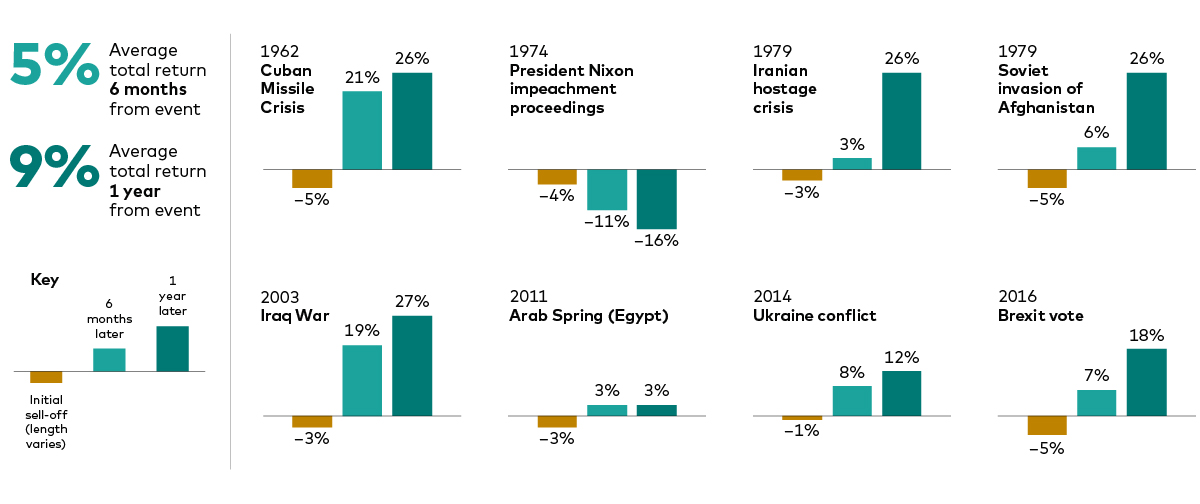

Geopolitical sell-offs have often been short-lived

Notes: Returns are based on the Dow Jones Industrial Average to 1963 and the Standard & Poor’s 500 Index thereafter. All returns are price returns and expressed in US dollar terms and do not include investment costs. Not shown, but included in the averages, are returns after the following events: the Suez Crisis (1956), construction of the Berlin Wall (1961), assassination of President Kennedy (1963), authorisation of military operations in Vietnam (1964), Israeli-Arab Six-Day War (1967), Israeli-Arab War/oil embargo (1973), shah of Iran’s exile (1979), US invasion of Grenada (1983), US bombing of Libya (1986), First Gulf War (1990), President Clinton impeachment proceedings (1998), Kosovo bombings (1999), September 11 attacks (2001), multi-force intervention in Libya (2011), US. anti-ISIS intervention in Syria (2014), and President Trump impeachment proceedings (2019 and 2021).

Sources: Vanguard calculations, as at 31 December 2021, using data from Refinitiv.

As the illustration shows, it hasn’t taken long for equity markets to recover from initial sell-offs in response to geopolitical events. Yet we wouldn’t have predicted such quick recoveries near the onset of any of these historical sell-offs. Nor do we predict one now as markets digest fast-moving developments related to Ukraine. Rather, we want investors to remain aware of the risks.

A new challenge for markets and policymakers

Inflation, already accelerating to multi-decade highs, may have impetus to climb further still, beyond Vanguard’s previous expectations, as the supply of goods from the region is constricted. Higher energy prices coupled with a potentially more challenging business environment owing to the conflict could weigh on economic growth and corporate profits. As a result, equity markets may respond poorly in the short run.

Our economic and market outlook for 2022 discussed the challenges we expected for policymakers who aimed to promote still-fragile Covid-19 economic recoveries and stifle worrisome inflation. The uncertain events in Ukraine make the policy calculus, especially for interest-rate-setting central banks, more problematic than it had been.

Invariably, the markets will test investors’ resolve yet again. Such environments may prompt investors to abandon well-considered asset allocations and encourage them to try to time the market, somehow picking not only the right time to exit, but also the right time to get back in.

Instead, we encourage advisers to help their clients maintain discipline and focus on what they can control, one of the tenets of Vanguard’s Principles for Investing Success. They’re what keep investors, in the long run, still standing.

Geopolitical sell-offs are typically short-lived

Share the geopolitical impact chart shown above with your colleagues and clients.

Open PDF