- Environmental, social and governance - or ESG - ratings are increasingly used in investment products either at the initial construction phase or as part of the ongoing management process.

- However, the relationship between ESG ratings and portfolio returns is still not well understood.

- In a recent study, we explored the investment implications by using ratings from three well-known ESG data providers.

“Similar to our findings at the individual stock level, at the portfolio level, we found no persistent link between the differences in risk and return between portfolios constructed using ESG ratings as selection criteria and the underlying market.”

Head of ESG research

Many investment products consider environmental, social and governance (ESG) ratings, either at the initial construction phase or as part of the ongoing management process. But what are the investment implications of using ESG ratings?

We looked into the link between ESG ratings from three well-known ESG ratings providers and equity performance to try and answer this question.

ESG sub-categories vary between ratings providers

As a first step, we mapped ESG ratings from LSEG (formerly Refinitiv), MSCI and Sustainalytics to a universe of US equities, as represented by the constituents of the Russell 3000 index1. The information that goes into these ratings can differ quite significantly across the providers. While all three have the same top-level pillars of E, S and G, they differ when it comes to the underlying categories, themes and issues that make up these pillars.

For example, LSEG breaks the E, S and G into 10 ‘categories’, which are then further divided into 25 ‘themes’; MSCI breaks ESG into 10 ‘themes’, which are made up of 35 ‘key issues’; and Sustainalytics divides ESG into 52 ‘issues’.

No clear link between ESG ratings and stock performance

At the individual stock level, we found the link between E, S and G ratings and stock price performance to be very inconsistent. Across our analysis, some findings indicated no link, some indicated a positive link and one indicated a negative link between E, S and G ratings and performance. What’s more, small adjustments to the scope of our analysis, such as changing the time period observed, often led to substantial changes in the results.

Relevance of style factors detected

We constructed nine portfolios for each of the environmental, social and governance categories based on the ratings of each provider. These portfolios differed from one another by the restrictiveness of the ESG-related filter applied.

In the least restrictive case, we selected companies rated within the top 90% of ratings of each industry-year. In the most restrictive case, we selected only the top 10% in each industry-year. In between these two extremes, we moved in 10% increments. The remaining stocks were then weighted according to their market capitalisation at the end of each month.

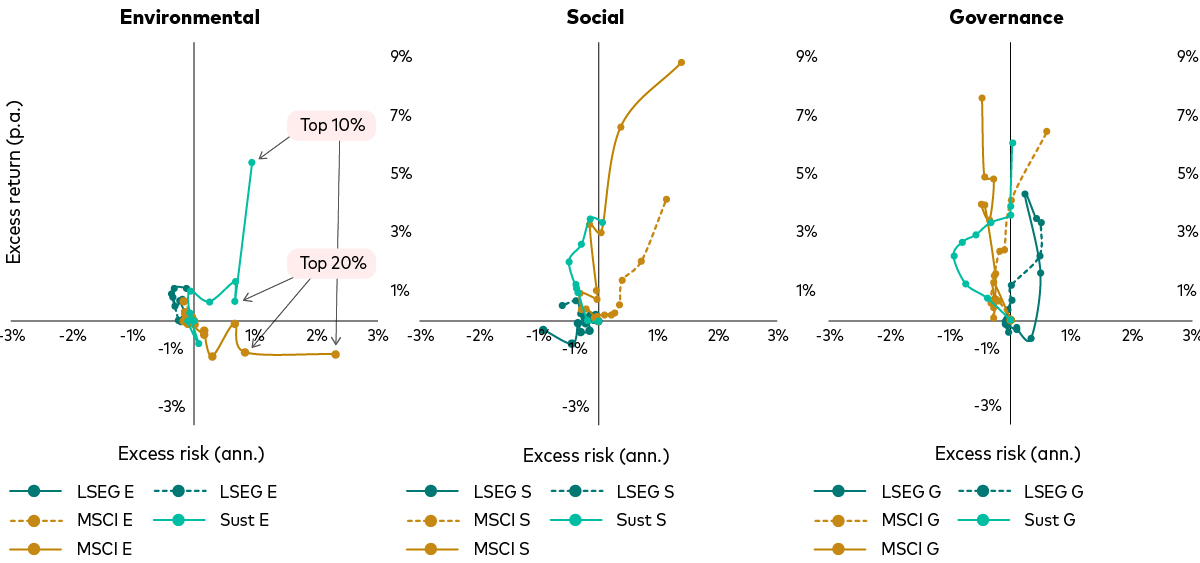

Similar to our findings at the individual stock level, at the portfolio level, we found no persistent link between the differences in risk and return between portfolios constructed using ESG ratings as selection criteria and the underlying market, as the charts below illustrate.

In our study we were looking for trends in terms of risk and reward. The lines connecting the dots represent the different portfolios. Notably, the top-left quadrant is where returns are higher and volatility is lower. The bottom right quadrant is where returns are lower and volatility is higher. As we can see, no clear pattern has emerged, which means that there is no consistent outcome for portfolios where ESG ratings have been used to select stocks.

No consistent link between E, S and G ratings-based stock selection and portfolio performance

Past performance is not a reliable indicator of future results.

Notes: The table displays raw differences in annualised returns and standard deviations between portfolios formed based on the Russell 3000 by selecting only those companies that belong to the top [x]% in each industry-year given their respective E, S and G scores from providers LSEG, MSCI and Sustainalytics. Time period observed:1 January 2019 to 31 December 2022, represented by the solid lines, and 1 January 2013 to 31 December 2022, represented by the dotted lines. Return data is calculated in USD (total return) with daily frequency.

Sources: Calculations based on data from LSEG, MSCI, Sustainalytics and FactSet, USD, for the periods 1 January 2019 to 31 December 2022 and 1 January 2013 to 31 December 2022.

However, when it came to style factor exposures2, we found that selecting stocks based on ESG ratings tended to lead to a bias towards the large-cap, profitability, investment and momentum factors. Furthermore, these biases tended to intensify the more restrictive (i.e., the more ESG focused) the selection became.

After removing the effect of these style factors, we found an increase in returns relative to the market only among a few of the most selective, least diversified ESG portfolios.

Understanding the investment implications of ESG ratings

So what are investors to take from our findings?

At the single stock level, we found the link between E, S and G ratings and performance to be very inconsistent. When these ratings are used to construct equity portfolios however, the picture becomes clearer. Our analysis highlights the relevance of traditional style factors in explaining portfolio returns – a relevance that tends to increase, the stronger the focus on E, S or G is in the portfolio.

Investors may want to consider whether the exposure to such factors may help or hinder long-term performance. If investors want to mitigate such factor exposures, they should look for broadly diversified rather than concentrated portfolios. All in all, investors should take any portfolio-level decisions on a fund-by-fund basis.

1 While data from LSEG and MSCI was available as of our start year (January 2013), Sustainalytics’ ratings were only available from 2019. On this basis we ran the analysis twice, once based on a reduced sample size starting in January 2019 using LSEG, MSCI as well as Sustainalytics data (the core model), and once using only LSEG and MSCI data from 2013 (the extended sample). The cross-section of our core sample contained 726 stocks in January 2019 and 675 stocks in December 2022. Given that LSEG’s and MSCI’s data coverage is more extensive than that of Sustainalytics, the cross-section of the extended sample rose from 699 in January 2013 to 1,917 in December 2022.

2 In our model, we used the style factors size, value, profitability and investment based on Fama and French (2015) and momentum from Carhart (1993).

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Past performance is not a reliable indicator of future results.

Performance may be calculated in a currency that differs from the base currency of the fund. As a result, returns may decrease or increase due to currency fluctuations.

Important information

For professional investors only (as defined under the MiFID II Directive) investing for their own account (including management companies (fund of funds) and professional clients investing on behalf of

their discretionary clients). In Switzerland for professional investors only. Not to be distributed to the public.

The information contained in this document is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information in this document does not constitute legal, tax, or investment advice. You must not, therefore, rely on the content of this document when making any investment decisions.

The information contained in this document is for educational purposes only and is not a recommendation or solicitation to buy or sell investments.

Issued in EEA by Vanguard Group (Ireland) Limited which is regulated in Ireland by the Central Bank of Ireland.

Issued in Switzerland by Vanguard Investments Switzerland GmbH.

Issued by Vanguard Asset Management, Limited which is authorised and regulated in the UK by the Financial Conduct Authority.

© 2023 Vanguard Group (Ireland) Limited. All rights reserved.

© 2023 Vanguard Investments Switzerland GmbH. All rights reserved.

© 2023 Vanguard Asset Management, Limited. All rights reserved.